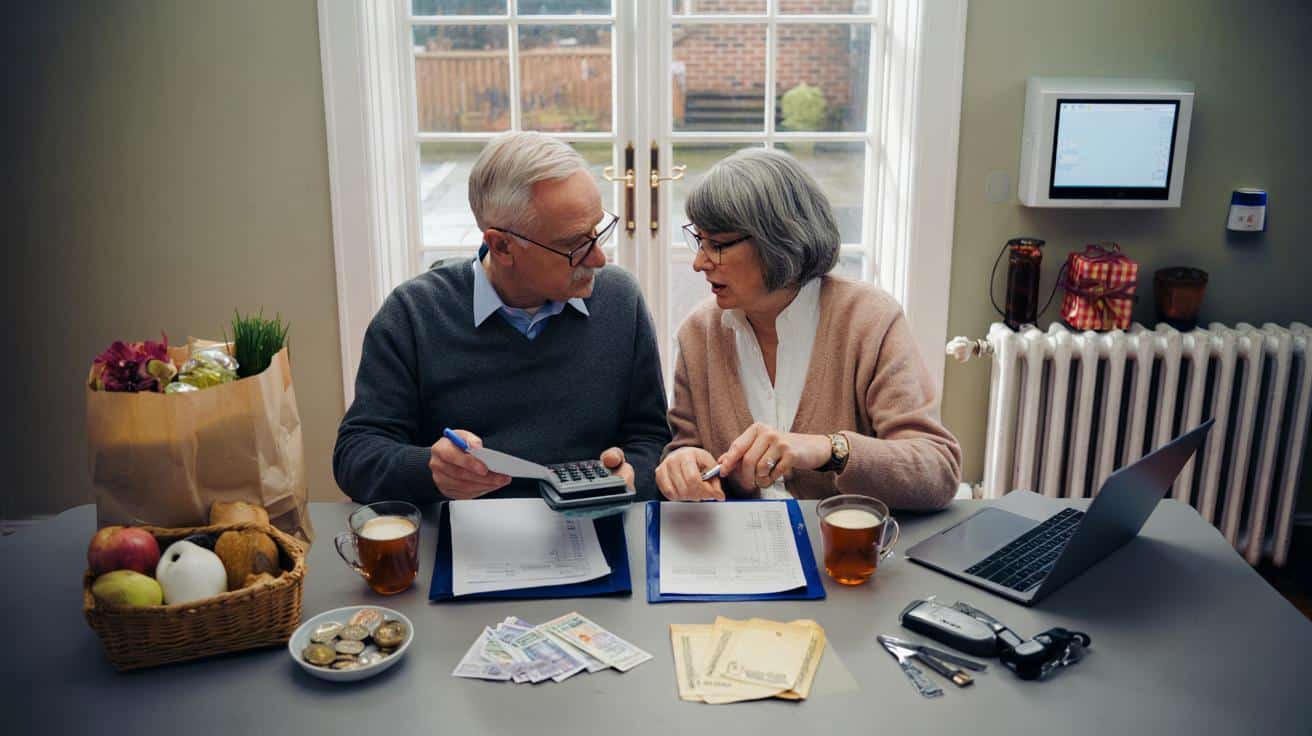

Here is the monthly number hiding behind that feeling.

Cost pressures have not vanished, even as inflation cools on the headline. Energy use climbs in colder months, food remains pricier than a few years ago, and travel or family help often stays on the calendar. For many Britons reaching age 68, the big question is simple yet urgent. What does an average month actually cost.

A recent snapshot of retiree sentiment helps explain the mood. An Employee Benefit Research Institute survey finds 32% of retirees say their standard of living is lower in retirement than during their working years, while only 10% say it is higher. Almost half, 46%, think they did not save enough, and those who say current spending is more than they can afford rose from 17% in 2020 to 27% in 2022. That shift tells its own story.

The number that best fits a 68-year-old middle class couple

There is limited data that isolates spending exactly at age 68. But the Consumer Expenditure Surveys from the U.S. Bureau of Labor Statistics offer a useful proxy that can be mapped across ages. The survey counts spending for a “consumer unit” which usually functions like a household. For ages 65 to 74 the average unit size is 1.9 people, so figures roughly mirror a couple.

Within this framework, average annual spending for those aged 55 to 64 equates to about £68,400 when converted for UK readers, while the 65 to 74 group drops to roughly £53,400. If you assume the midpoints line up with ages 60 and 70, that implies a 21.9% decline over the decade. Smoothed year by year, it works out at a compounding decline of 2.44%.

Apply that glide path to a couple aged 68 and you land near £56,100 a year. On a monthly spending basis, that sits at around £4,680. The exact slope depends on household size, but this is in the right ballpark for an average middle class retiree couple at 68.

What sits inside that monthly budget in the UK

Spending patterns vary by region and lifestyle. Yet the big building blocks for a British household at 68 rarely surprise. The colder months add a seasonal tilt to the mix, especially for those in draughty homes or on standard energy tariffs.

- Housing costs and Council Tax, energy and water, groceries and household goods, transport and insurance, healthcare and dental, gifts and family support, leisure and small trips

Those categories shuffle as work-related costs fade and home-focused living grows. Some outlays fall as mortgages end or commuting stops. Others rise with age, like health and care, or simply shift to keep up hobbies and visits to adult children and grandchildren.

The survey signals that show why money feels tighter

The EBRI survey points to a cautionary reset. Thirty-two percent of retirees report a lower standard of living than before they stopped work, compared with just 10% who report a higher one. In parallel, 46% believe they did not save enough for retirement. And the share saying their current spending is more than they can afford moved from 17% in 2020 to 27% in 2022, the most recent survey year in the study.

Those numbers resonate in Britain too, where winter energy use lifts bills just as festive spending looms. Middle incomes often earn too much for broad support yet not enough to feel cushioned. That is why knowing the ballpark figure near £4,680 a month for a 68-year-old couple matters. It frames choices before costs snowball.

How to make that figure work harder without big compromises

No single lever fixes everything, but small moves stack up. Start with an honest audit of recurring debits, trim underused subscriptions, and check whether a different supermarket basket or own-label swap eases the weekly shop. Energy use is worth a fresh look in winter, from heating schedules to room-by-room controls, because a few kilowatt-hours saved each day add up over a month.

Some retirees also top up income from home-based work that fits around health and caring duties. Even a modest amount can offset rising essentials and keep discretionary spend alive for travel or hobbies. And it helps to ringfence a buffer for irregular costs, since todays “extras” often arrive all at once.

Method note for readers. The spending estimates above draw on the Consumer Expenditure Surveys age bands, assuming the midpoint method and a 2.44% annual decline between ages 60 and 70, then converting to pounds for clarity. Figures refer to a consumer unit averaging 1.9 people in the 65 to 74 cohort, which aligns with a couple in practice. Currency conversion is approximate.